This is the first of a 3-part series that takes a look at the evolution of cryptocurrency and the problem with money today. The 1st part of this series of articles addresses the multiple failures of money today, while the 2nd part explains how cryptocurrencies address these issues and rectify them. Part 3 is an inside look at the strengths of cryptocurrencies over traditional money and what the future holds for both. This series of articles is intended for beginners with zero knowledge of economics, finance and crypto.

The Problem With Money Today

Cryptocurrency, or crypto as it is often referred to, is the answer to a long-standing problem with finance and money.

What problem? you ask. I’ve got no problem with money at all today apart from not having enough of it.

The problem with fiat money is that it rewards the minority that can handle money, but fools the generation that has worked and saved money.

— Adam Smith

But the matter of fact is you do have a problem with it. You do, I do and everyone else does but we’ve become so accustomed to ‘that’s the way it’s always been done’ that we’ve become blind to its flaws. In order to understand the value proposition of cryptocurrencies, we first need to understand these specific problems they solve. (Read more: 4 Reasons Why Now is the Best Time for You to Invest in Cryptocurrencies)

Modern finance is broken. Just ask any banker you know if he understands where does the currency of his country get its value from. The US dollar, the ‘gold standard’ of foreign currency holdings, used to be pegged to actual gold bullion held by the US Treasury; there was an underlying asset that was tied to its value. However, in 1971, the relationship between gold and the US dollar, was cut. Interestingly enough since the metaphorical divorce of gold and US dollar value, both assets have had an inverse relationship. Keep this in mind, it’s an important point that we will revisit later in Part 2.

In the absence of the gold standard, there is no way to protect savings from confiscation through inflation. There is no safe store of value.

— Alan Greenspan, Chairman of US Federal Reserve, 1987–2006

Evolution of Money

Inverse relationship between gold and US

What’s obviously frightening, however, is the fact is that the entirety of the finance industry runs on the assumptions of price, of supply and demand, and not of intrinsic value. So, where does currency get its value from? This article by Chris Mayer covers it quite succinctly: tax credit. Governments are unable to fund their spending with tax revenue alone, so they print more money in order to make up for whatever shortfall they have.

However, if print money endlessly, you debase the value of your own currency by creating a never-ending increase in supply, thereby driving the price down. There’s nothing stopping the citizens, businesses and forex traders from selling off your useless currency in exchange for something that would serve as a better store of value (e.g. necessities or commodities or even other currencies, and trading with that).

We don’t have to look far for such examples; in third world countries like Cambodia or Vietnam, USD is widely accepted and even preferred by businesses despite each country having their own currencies of Riel and Dong respectively. Or in the past, when episodes of hyperinflation due to excessive money printing such as in the case of the German Weimar Republic, people turned to using American cigarettes as currency.

The U.S. government has a technology, called a printing press (or today, its electronic equivalent), that allows it to produce as many U.S. dollars as it wishes at no cost.

— Ben Bernanke, Chairman of US Federal Reserve 2006–2014

Thus, in order to ensure that citizens and businesses continue to use the local currency as legal tender, governments employ a trick. They demand payments for tax liabilities in the currency of their own country.

As taxation often scales proportionately to the amount of profits made by companies or individuals, it then makes sense to collect payment in that specific currency instead of turning to an alternative. Tax liabilities give currency value: All fiat money, or money issued by governments that do not possess an intrinsic value, essentially serve as tax credit.

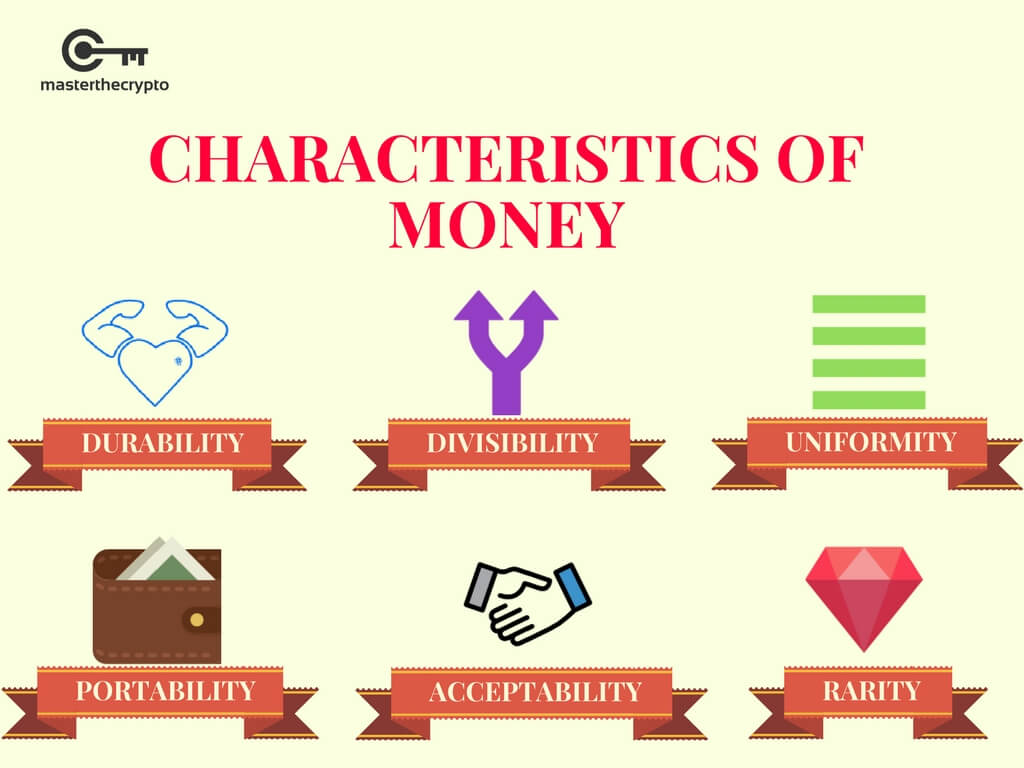

That’s not all, however, finance is more than just governments and the money they issue alone. Money cannot exist in a vacuum without an ecosystem of financial services. All this because money must have some characteristics (in order to be considered money) which necessitate the existence of banks:

While we can accept that the dollar notes in our wallets are respectably durable, portable, divisible, uniform and accepted, we all know that it is not infinitely so.

After passing through sufficient hands, dollar bills will start to suffer wear and tear. There’s a limit to how many dollar bills you can bring to you on a trip out to the market or to take an extreme example, buy a house. There’s a limit to how many merchants are going to be willing to accept 100 pennies as a dollar regardless of their equal value. Due to reprints and different minting years, not all dollar bills are going to look alike and last but not least, if you have had experience with US 2 dollar bills, UK 50 pound bills, or 500 Euro bills, you’d know universal acceptability is not true, let alone using your home currency in another country. (See also: Guide to Cryptocurrency Wallets: Why Do You Need Wallets?)

Hence, the only way we can actually use large, specific amounts of money easily, yet allows it to universally accepted and transacted in is to have a trusted storage provider who can offer credit and debit services.

In other words: Banks.

Banks act as trusted storage providers who provide us other services such as providing credit notes or direct debit to suppliers of goods and services. They enable us to store large amounts of money that we would be physically unable or would be unreasonably difficult to store ourselves. Without the worry of them ever running away with our money, right?

Not really.

Banks are, unfortunately, profit maximising entities, who we trust to manage our money. We trust them to not misuse the funds we store with them, and not to debase the currency. But wait, if they are profit maximising entities, doesn’t this mean that we would need to pay them for their services?

It is not from the benevolence of the butcher, the brewer, or the baker that we expect our dinner, but from their regard to their own interest.

— Adam Smith

Well, if it only that simple. The truth is that purely currency storing services did not exist except in the Roman empire; monasteries, nunneries and temples offered storage services for money and valuables in times of war. The original type of banks evolved mainly from money lenders who required funds to run their businesses or government official providing land to their serfs for farming. Lending and banking have been intertwined since their conception.

In other words, banks won’t charge you for the amount of money you store with them because that would decrease your overall savings over time which is exactly what you’re trying to avoid. Instead, they’d even offer you interest to keep your funds with them, on the premise that you need to trust them to secure your funds, knowing that they are going to conduct loans with your money. Thus, as profit maximising entities, the entire aim of banks is to make money off your money. How? By creating new money. (See also: When Trust is No Longer an Issue)

Wait! That doesn’t make any sense! Only governments can create new money!

Well, yes and no. The way banks create money is not via printing, the way they create money is via debt. Loans don’t exist in a vacuum; unless they’re from family or friends, loans most likely have an interest element to them. By storing money in a bank, you are as well, providing the bank with a loan. One that is of unknown duration to the bank, as you may withdraw your money at any time. This is the rationale given for lower interest rates on savings accounts vs loans as loans from banks to businesses or individuals have some kind of clause built in for a maximum repayment period. Interest on loans is a form of money creation, as the loans themselves can be packaged into different financial instruments and resold, creating money where it did not exist in the first place; this was exactly what happened in the 2008 Subprime Mortgage Crisis.

Speaking of which, we have seen time and time again we cannot trust banks: The 1997 Asian Financial Crisis, the 2001 Dotcom Bubble and most recently, as mentioned above, the 2008 Subprime Mortgage Crisis which directly led to the 2010 European Sovereign Debt Crisis. Each time caused by banks and the financial industry abusing the trust we place in them. Yet when dealing with fiat currency, we have no choice but to use banks, because no other institution is so firmly entrenched in the worldwide economy.

The root problem with conventional currency is all the trust that’s required to make it work. The central bank must be trusted not to debase the currency, but the history of fiat currencies is full of breaches of that trust. Banks must be trusted to hold our money and transfer it electronically, but they lend it out in waves of credit bubbles with barely a fraction in reserve. We have to trust them with our privacy, trust them not to let identity thieves drain our accounts.

— Satoshi Nakamoto

In Summary

Governments and banks, cannot be trusted to not debase money because they have done and will continue to do that.

So how do we solve this crazy problem? Stop using money entirely and trade in cows and horses like people did in the past?

In 2008, a pseudonymous cryptography researcher known only to the world as Satoshi Nakamoto, came up with an answer to that problem. That answer was Bitcoin.

You might also be interested in A Guide To Fundamental Analysis For Cryptocurrencies & Coins, Tokens & Altcoins: What’s the Difference?

This series is contributed by Bryan Chia, a tech/blockchain writer who is fascinated by cryptocurrencies and their revolutionary technology.

Get our exclusive e-book which will guide you through the step-by-step process to get started with making money via Cryptocurrency investments!

You can also join our Facebook group at Master The Crypto: Advanced Cryptocurrency Knowledge to ask any questions regarding cryptos!

I like cats. I write about stuff that I'm interested in, topics may vary greatly but flavor of the month is cryptocurrency and blockchain tech.